the sanmar group

Where Integrity Meets Excellence

Where Integrity Meets Excellence

Choose the Font :

Shaped by short - termism

Budget 2000 - 2001

By S Swaminathan

Yashwant Sinha is no novice to the art of budget-making. A former bureaucrat in the Finance Ministry himself, he was in the very vortex of crisis management in 1990-91 as Finance Minister in the Government led by Chandrasekhar. Later after the Bharatiya Janata Party (BJP) formed the coalition Government at the Centre in 1996, he has moulded three successive budgets including that for 2000-2001. His latest offering has come as a largely missed opportunity for fashioning fiscal policy as a powerful catalyst for mainstreaming India as a vibrant participant in the emerging global economic thoroughfare.

Much more than a failure of expectations, Sinha’s third budget reveals a clear failure of design to the extent that it has not leveraged on the strong fundamentals of the Indian economy in evidence during the current year, 1999-2000 .

Economic backdrop for budget

The Economic Survey 1999-2000 which was tabled in Parliament by the Government on the eve of presentation of the Budget for 2000-2001, offers a portrait of the economy as it is emerging from a three-year long slow-down in industrial production mainly owing to a demand recession.Even though the growth rate for Gross Domestic Product (GDP) during 1999-2000 has been estimated at only 5.9 per cent (as compared to 6.8 per cent in the previous year), the indications of a revival of industrial growth (at 6.2 per cent for April-December 1999-2000 as compared to a dismal 4.0 per cent for the whole fiscal year 1998-1999) are indeed strong. A slump in agricultural performance (a decline by 2.2 per cent) after a year of spectacular growth at 7.4 per cent seemed to suggest the GDP growth rate ought to have been much higher if the blip in agricultural production had not occurred.

The Economic Survey 1999-2000 which was tabled in Parliament by the Government on the eve of presentation of the Budget for 2000-2001, offers a portrait of the economy as it is emerging from a three-year long slow-down in industrial production mainly owing to a demand recession.Even though the growth rate for Gross Domestic Product (GDP) during 1999-2000 has been estimated at only 5.9 per cent (as compared to 6.8 per cent in the previous year), the indications of a revival of industrial growth (at 6.2 per cent for April-December 1999-2000 as compared to a dismal 4.0 per cent for the whole fiscal year 1998-1999) are indeed strong. A slump in agricultural performance (a decline by 2.2 per cent) after a year of spectacular growth at 7.4 per cent seemed to suggest the GDP growth rate ought to have been much higher if the blip in agricultural production had not occurred.

Within industry, manufacturing appeared to have overcome the inertia of the previous two years with a 7 per cent growth. “Construction” emerged as a key growth sector during 1999-2000 with an estimated growth rate of 9 per cent (as compared to 5.7 per cent in 1998-99).Given the structural transformation of the economy since 1991, it is not surprising that the services sector is emerging as a major contributor to the GDP accounting for as much as 51.2 per cent in 1998-99. In 1999-2000, this sector recorded a growth of 8.2 per cent with the sub-sector “Financial services” registering a growth of 10.5 per cent (as compared to 6.1 per cent in the previous year).

The year 1999-2000 turned out to be an unprecedented period of low inflation for the Indian economy with the average annual rate of inflation almost pegged at 3 per cent as against 6.9 per cent in the previous year and 10.9 per cent in 1994-95. It is still an unsettled dispute among economists whether the low rate of inflation captured by the Wholesale Price Index is a statistical illusion or an aberration given the expansion in Broad Money Supply (M3) of the order of 12-13 per cent during the year.

The year 1999-2000 turned out to be an unprecedented period of low inflation for the Indian economy with the average annual rate of inflation almost pegged at 3 per cent as against 6.9 per cent in the previous year and 10.9 per cent in 1994-95. It is still an unsettled dispute among economists whether the low rate of inflation captured by the Wholesale Price Index is a statistical illusion or an aberration given the expansion in Broad Money Supply (M3) of the order of 12-13 per cent during the year.

Nevertheless the reality of a comfortable supply position with regard to primary articles and manufactured products and the increasing pressure on margins in industry emanating from growing competition in markets triggered by import liberalisation seemed to validate the belief that low inflation is fast becoming an integral feature of the restructured economy.

As Finance Minister, Yashwant Sinha could not have bargained for a more resilient Balance of Payments situation than what the year 1999-2000 had yielded. Despite the East Asian economic crisis of 1997-98 and the sanctions clamped down on India by the US in the wake of Pokhran-II nuclear tests, the forex reserves continued to rise with a net accretion by $2.4 billion during April 1999-January 2000. Export growth at around 12 per cent for the year (as against a decline by 4 per cent in 1998-99) and significant improvements in portfolio investment and non-resident deposit inflows combined with a moderate import growth of about 9 per cent had ensured that the total forex reserves at about $35 billion provided ample cushion for imports covering as much as 8 months’ import commitments. The Rupee stayed strong and stable throughout the year range-bound between 43.30 and 43.60 as against the US dollar.

The flip side

Economic Survey 1999-2000 is not all Hosannas to the Indian economy. Apart from the dip in agricultural production, there were areas of concern which the survey depicted in candid detail. All was not well on the savings front. In 1998-99, Gross Domestic Savings had declined to 22.3 per cent of the Gross Domestic Product, from 24.7 per cent in 1997-98. The Investment Rate in the economy had suffered as a result.

From 26.2 per cent in 1997-98, it came down to 23.4 per cent in 1998-99. The implication clearly was that the growth rate in the economy (around 6 per cent) could not be sustained without the reactivisation of investment. Apart from the decline in domestic capital formation, what was causing concern was the none-too robust outlook for Foreign Direct Investment (FDI) inflows.

Challenging as these deficiencies were, the central issue which called for concerted attention was the chronic fiscal imbalance – the plight of the Centre and the States caught as they were between snowballing expenditure and stagnant revenue receipts. The Survey underscored fiscal correction as the precondition for accelerating economic growth. There was little quibbling that “hard decisions on many fronts” would be needed for putting the fiscal system back on its feet. This language of “hard decisions” has been reverberating through the corridors of power in New Delhi for weeks before Sinha unravelled his budget.

But then weeks after the event, analysts continue to wonder where these “hard decisions” reside in the budget. To say that Sinha’s package of tax proposals has produced consternation in corporate circles is not to go along with the fiction that his is a tough-minded budget.

Budget in the three segments

The belief that a budget is a logical construct with an overarching economic design might appear to be an idealist approach to what perhaps can only remain a string of numbers backed by the dominant instinct of political survival. But then an analysis of a budget cannot properly turn on political motivation but should be anchored in the premise that it is a financial plan articulating a pattern of preferences and compulsions of a Government in action. Considered this way, there are three broad segments of the budget which merit close scrutiny.

These are:

1. The expenditure plan with its priorities

2. The strategy for resources mobilisation through taxes and other revenue receipts and

3. The management (or mismanagement) of the resources gap through deficit financing, tolerable or otherwise.

Sinha’s expenditure blueprint

Contrary to the catechism which the Finance Minister has all along been treated to, he has simply not been able to tame expenditure. The budget for 2000-2001 entails a total spending of Rs.3384.87 billion – an increase by a seemingly modest 11.5 per cent – compared to Rs.3037.38 billion in 1999-2000. The complexion of the plan changes when the inexorable phenomenon of overshooting of expenditure is reckoned with. Last year, Sinha projected a total expenditure of Rs.2838.82 billion whereas the actual expenditure exceeded the estimate by around 7 per cent. In absolute terms, what the new budget envisages is an increase of Rs.348 billion in total expenditure. The breakdown of the incremental expenditure is as follows:

Contrary to the catechism which the Finance Minister has all along been treated to, he has simply not been able to tame expenditure. The budget for 2000-2001 entails a total spending of Rs.3384.87 billion – an increase by a seemingly modest 11.5 per cent – compared to Rs.3037.38 billion in 1999-2000. The complexion of the plan changes when the inexorable phenomenon of overshooting of expenditure is reckoned with. Last year, Sinha projected a total expenditure of Rs.2838.82 billion whereas the actual expenditure exceeded the estimate by around 7 per cent. In absolute terms, what the new budget envisages is an increase of Rs.348 billion in total expenditure. The breakdown of the incremental expenditure is as follows:

An interesting aspect of the increase in expenditure planned for 2000-2001 is that almost 81 per cent of the increase relates to revenue expenditure at a time when government investments in infrastructure are crucially needed to upgrade the economy. Looking at it differently, of the increase in total expenditure of Rs.348 billion, only Rs.76 billion represent the budgetary allocation for what is called “Central Plan Outlay” – a term which effectively misleads public perception into believing that such items of expenditure carry special virtues of strictly-prioritised categories of spending!

Strategy for resources mobilisation

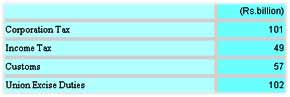

As against an incremental expenditure of Rs.348 billion for the year, Sinha’s budget anticipates additional net tax revenue of Rs.197 billion. What is involved here is the principle of tax devolution in a federal polity according to which the Union Government is the fountain-head for tax resources mobilisation with the corresponding obligation to share the tax proceeds with the State Governments. Sinha’s budget provides for a total increase in Gross Tax Revenue by Rs.303 billion of which the State Governments are to have a share to the extent of Rs.106 billion (or about 54 per cent).

The breakdown of the increase in the Gross Tax Revenue projected in the budget is as follows:

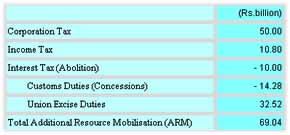

It should be noted that of the total increase in Gross Tax Revenue of Rs.303 billion, only Rs.69 billion constitute Additional Resource Mobilisation (ARM), the balance being derived from the growth factor in the economy. If the assumption is that GDP growth next year will be 7 per cent and that inflation will rule at 4 per cent, a Gross Tax Revenue projection of about Rs.1905 billion, would be in order. The Finance Ministry’s projection of Rs.2003 billion of Gross Tax Revenue could well prove over-optimistic. That apart, the prospect of direct taxes (Corporation Tax and Income Tax) contributing only 36 per cent of the Gross Tax Revenue compared to 64 per cent being accounted for by commodity taxes offers its own comment on the largely unfinished agenda of tax reforms.

The overall effect of the budget proposals regarding taxation is as follows:

The economics of the tax proposals

Yashwant Sinha has not put forth any elaborate rationale for the tax proposals introduced in the budget excepting a bland statement that he has attempted an equitable distribution of the tax burden among the different segments of the population. Even granting that the budget is not particularly premised on the objective of raising the ratio of direct tax revenue to the gross domestic product, it is difficult to erase the impression that the tax proposals are mainly targeted at the corporate sector.

The five year phasing-out of tax exemption of export earnings is not part of tax reforms but is rather a belated recognition of its incompatibility with the WTO mandate.The reduction in the rate of tax under the scheme of Minimum Alternate Tax (MAT) from an effective 10.5 per cent of the book profits to 7.5 per cent with the exclusion of export profits similarly does not represent any march towards rationalisation of the tax regime. The more controversial aspect of the proposals regarding corporate taxation is the move to increase the tax on distributed profits of domestic companies from 10 to 20 per cent.Even if a restraining impact is claimed for the proposal as regards the tendency for corporates to distribute largesse to shareholders, the

question of needless discrimination against domestic companies cannot be overlooked. All this apart, the decision to continue with the surcharge on income tax and corporation tax and to raise the surcharge to 15 per cent in the case of personal incomes above Rs.1.5 lakh cannot be too strongly deprecated on ethical grounds.

Contrary to the strong economic case for utilising the transition period under the WTO dispensation for operating relatively high tariffs on imports in the wake of termination of Quantitative Restrictions on a wide range of imports, the Finance Minister seems to have plumped for a more fashionable low-tariff regime. The result is not only a tax give-away of Rs.14.28 billion on customs but also an overall moderate growth of anticipated Customs Revenue at Rs.535.72 billion or by 12 per cent. The rationalisation of the Excise Duty Structure through the introduction of a single rate Central Value Added Tax (CENVAT) at 16 per cent in the place of the three existing rates of 8 per cent, 16 per cent and 24 per cent would have been a progressive reform but for the decision to live with the special Excise Duty with a three-tier structure. Indications of an assessee-friendly Excise Duty regime are not however lacking. Payments from 1 July, 2000 of Excise Duty in fortnightly instalments instead of on a day-to-day basis and the decision to dispense with statutory excise records are moves in the right direction.

Contrary to the strong economic case for utilising the transition period under the WTO dispensation for operating relatively high tariffs on imports in the wake of termination of Quantitative Restrictions on a wide range of imports, the Finance Minister seems to have plumped for a more fashionable low-tariff regime. The result is not only a tax give-away of Rs.14.28 billion on customs but also an overall moderate growth of anticipated Customs Revenue at Rs.535.72 billion or by 12 per cent. The rationalisation of the Excise Duty Structure through the introduction of a single rate Central Value Added Tax (CENVAT) at 16 per cent in the place of the three existing rates of 8 per cent, 16 per cent and 24 per cent would have been a progressive reform but for the decision to live with the special Excise Duty with a three-tier structure. Indications of an assessee-friendly Excise Duty regime are not however lacking. Payments from 1 July, 2000 of Excise Duty in fortnightly instalments instead of on a day-to-day basis and the decision to dispense with statutory excise records are moves in the right direction.

Non-tax revenue

The receipts under this head are projected to increase to Rs.574.64 billion in 2000-2001 from Rs.530.35 billion in 1999-2000 or by about 8 per cent. The major constituents of non-tax revenue are Interest Receipts, Dividends and Profits. While Interest Receipts are expected to increase to Rs.367.21 billion in 2000-2001 from Rs.341.44 billion in 1999-2000, Dividends and Profits are projected to grow from Rs.93.10 billion in 1999-2000 to Rs.112.04 billion next year or by about 20 per cent. It must be noted, however, that in 1999-2000, Dividends and Profits (reflecting the performance of Public Sector Enterprises and financial institutions including nationalised banks) actually showed a short fall of 2.2 per cent in terms of the budgeted figure of Rs.94.82 billion. This was mainly because the “surplus profits” of the Reserve Bank of India were down to Rs.45 billion as against the projection of Rs.57 billion.

The receipts under this head are projected to increase to Rs.574.64 billion in 2000-2001 from Rs.530.35 billion in 1999-2000 or by about 8 per cent. The major constituents of non-tax revenue are Interest Receipts, Dividends and Profits. While Interest Receipts are expected to increase to Rs.367.21 billion in 2000-2001 from Rs.341.44 billion in 1999-2000, Dividends and Profits are projected to grow from Rs.93.10 billion in 1999-2000 to Rs.112.04 billion next year or by about 20 per cent. It must be noted, however, that in 1999-2000, Dividends and Profits (reflecting the performance of Public Sector Enterprises and financial institutions including nationalised banks) actually showed a short fall of 2.2 per cent in terms of the budgeted figure of Rs.94.82 billion. This was mainly because the “surplus profits” of the Reserve Bank of India were down to Rs.45 billion as against the projection of Rs.57 billion.

Capital receipts

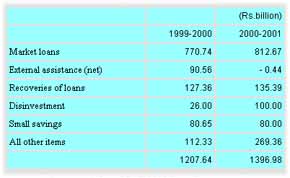

The central challenge of budgetary policy in India is to rein in revenue deficit and to apply capital receipts increasingly towards investments in the public sector even if the broad concept of downsizing of government comes to be earnestly implemented. The view that all forms of borrowing by the government need to be eschewed is a part of what is known as the Washington Consensus inspired by the IMF and the World Bank. In terms of the realities of infrastructural inadequacies in India and the remoteness of the expectation of large cascades of private investments flowing into infrastructure projects, the government will have to continue to make investments in this sector for years to come. The question is how the government can cope with this expectation so long as capital receipts are applied to the financing of the revenue deficit. In 2000-2001, total capital receipts of the order of Rs.1397 billion are anticipated. The breakdown is:

Given a projected revenue deficit of Rs.774.25 billion, there is no getting away from the fact that market borrowing will largely be used to offset the revenue deficit and that there will be little capital expenditure by way of investment in the public sector apart from an increase in the Defence Capital Outlay by Rs.53 billion.

Government of India Budgetary Trends

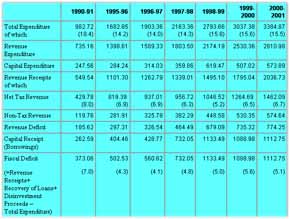

The accompanying table summarises the budgetary trends since 1990-91. If there is one central message which comes through the data, it is that Indian fiscal management has to be extricated from three serious deficiencies.

The accompanying table summarises the budgetary trends since 1990-91. If there is one central message which comes through the data, it is that Indian fiscal management has to be extricated from three serious deficiencies.

These are:

1. The preponderance of revenue expenditure totally disproportionate to the cost-effectiveness of governance,

2. The lag in tax revenue in relation to the growth in GDP since 1991 and

3. The gross failure of the policy makers to correct the distortions caused by a constellation of inefficient and bloated public enterprises.

The verdict on Sinha’s budget for 2000-2001 may sound harsh but the tragic failure to address questions of Savings and Investment and the critical need to accelerate economic growth as a necessary condition for improving the lot of the poor seems so obviously mirrored in the budget lost opportunity.The author is a well-known academician turned journalist and a former Economic Adviser to the Sanmar group.

Designed by  F5ive Technologies

F5ive Technologies